This is the inaugural post of my blog on biotech finance. With this post, I aim to accomplish three things:

- Identify the main challenge of the life sciences industry: the rising cost of drug development and decreasing R&D productivity

- Highlight overconfidence and deterministic thinking as cognitive biases that limit our ability to answer these challenges

- Propose a probabilistic model of capital allocation as the solution to rising R&D uncertainty and a novel source of active financial return (alpha)

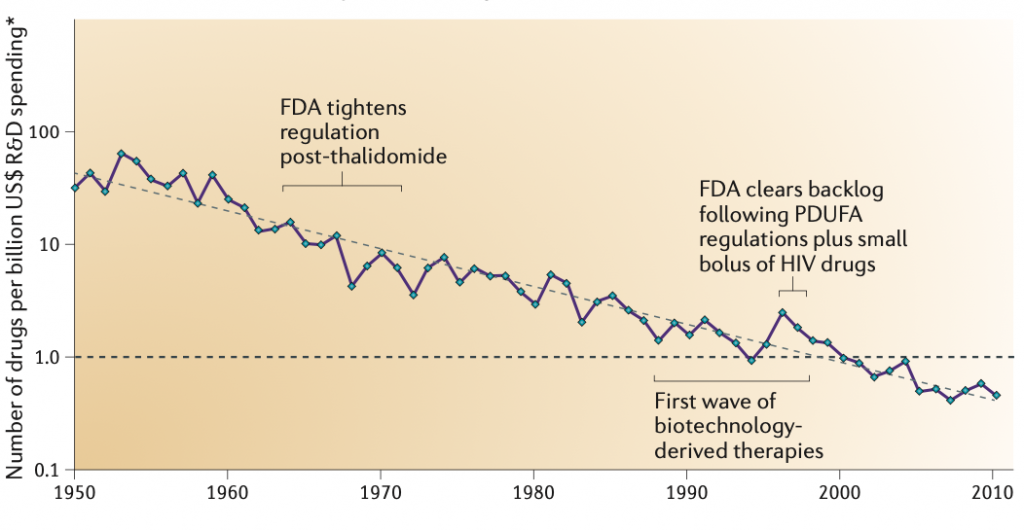

Eroom’s Law

Eroom’s law (Moore’s law spelled in reverse) is an observation that the cost of drug discovery has doubled every nine years from 1950 until 2010:

Figure 1. Pharmaceutical R&D Efficiency (Inflation-adjusted)

Scannell et al., who coined the term, list the following underlying causes as responsible for the observed trend:

Table 1. Hypothesized Causes of Eroom’s Law (Scannell et al.)

| Cause | Description |

|---|---|

| The ‘Better than the Beatles’ problem’ | An ever-improving back catalog of approved medicines raises the evidential hurdles for approval, adoption, and reimbursement |

| The ‘cautious regulator’ problem’ | Progressive lowering of the risk tolerance of drug regulatory agencies raises the bar for the introduction of new drugs |

| The ‘throw money at it’ tendency’ | The tendency to add resources to R&D has led to a rise in R&D spending without necessarily raising its productivity |

| The ‘basic research–brute force’ bias’ | The tendency to overestimate the ability of advances in basic research to increase the probability that a drug will be successful in clinical trials |

As you can tell from the elaborate problem names in the above table, the hypothesized reasons are complex. Each intertwines many economic, regulatory, scientific, and behavioral factors. To get a full appreciation for the complexity, I recommend that you read the original article.

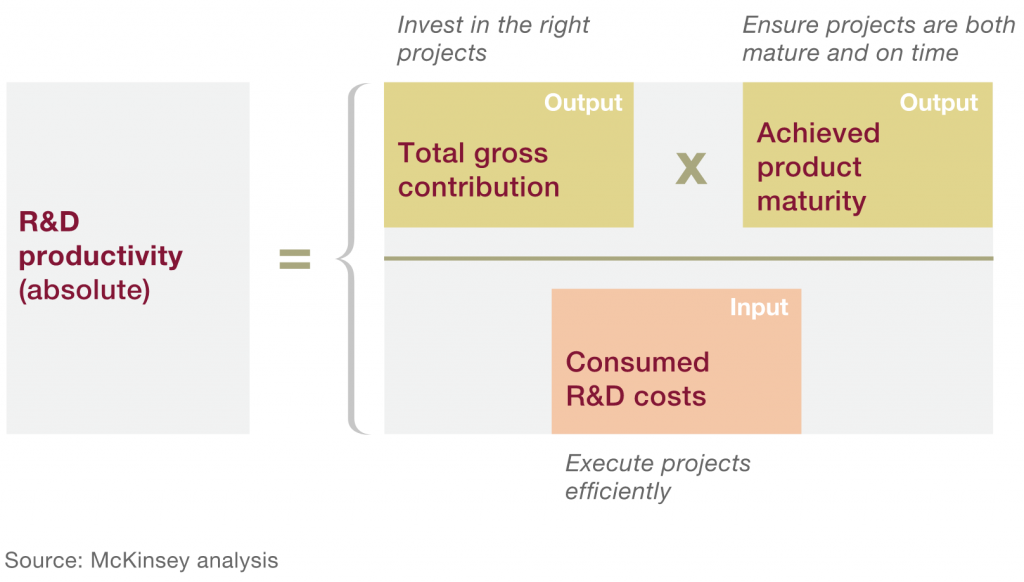

However, to facilitate the systematic analysis of the R&D efficiency problem, I prefer a more straightforward framework proposed by McKinsey & Co. In the words of McKinsey researchers: “Just as Alexander the Great is said to have undone the Gordian knot by the simple expedient of slicing through it with his sword—[…]—our formula makes relatively quick, simple work of a knotty problem.”

Here’s the formula:

Figure 2. Drivers of R&D Productivity

Eroom’s law in McKinsey terms

In essence, the four Eroom’s law causes in Table 1 can be generalized into two trends:

- New drug approvals progressively raise the bar for future drug candidates

- The ‘better than the Beatles’ problem’

- The ‘cautious regulator’ problem’

- Scientists and other decision-makers are prone to overconfidence bias that invites over-commitment of resources

- The ‘throw money at it’ tendency’

- the ‘basic research–brute force’ bias’

The first trend is, arguably, not that interesting from a process improvement point of view. Raising the standard of care is beneficial for the patient and in a way this is a good problem to have. The second trend, however, we are going to analyze in-depth.

First, let’s look at the above description of the second trend: “decision-makers are prone to overconfidence bias that invites over-commitment of resources”. Here, overconfidence is the operative word. Let’s describe the causes and consequences of this overconfidence in McKinsey terms of R&D productivity (costs, total gross contribution, and achieved product maturity):

Table 2. Overconfidence bias in McKinsey terms of R&D productivity

| Factor | Relation |

|---|---|

| R&D costs | Go up as a result of overconfidence bias |

| Total gross contribution (Project value) | Drives overconfidence, when overestimated |

| Achieved product maturity (R&D speed and success probability) | Same as above |

Again, the first line item above is more of a natural consequence rather than the cause. But let’s investigate what causes the scientists and investors to overestimate the project value and success probability.

Drivers of overconfidence

Let’s assume that the decision-makers’ extrinsic motivations (e.g. salary bonus, job security, promotional opportunities) are fully aligned with the success of the R&D project. This assumption is actually never true, and that is a subject of a separate future post. But for the purposes of this discussion, let’s limit the scope of our analysis to the factors intrinsic to the R&D project itself.

With that in mind, I see three potential reasons for overestimating the probability of success for a given R&D project:

- Lack of historical data needed to estimate the probability of success and the perceived economic value of the project

- Lack of the analytical capability needed to produce such estimates, as well as estimates of the associated probability distributions

- Deterministic thinking that supersedes the probabilistic nature of scientific research and de-emphasizes data modeling in decision-making

Let’s unpack each.

Lack of historical data

It would appear that the data for R&D success prediction is now widely available from sources, maintained by the National Institutes of Health, as well as a variety of commercial providers. However, because each new drug technology is, by definition, innovative, it is unclear how relevant the historical data context is for a given R&D project. Furthermore, as research tools become more advanced, new kinds of data become available. Such data immediately influences business decisions, even though its utility in increasing prediction accuracy has not yet been fully established. Oskamp (1965) points out that an increased amount of information may indeed increase the experts’ confidence in their prediction without necessarily improving its accuracy.

Lack of analytical capability

In 2020, there is no excuse for not finding analytical expertise. The bottleneck, however, is not in finding the data experts. It is what data to give them and, more importantly, what questions to ask. Both of those questions require some form of interdisciplinary thinking (e.g., life sciences, AI, finance) that is relatively rare.

Systematic analysis is also hindered by a persistent myth about biotech that to evaluate a project as an investment one needs to deeply understand the science behind it. Interestingly, this myth exists both within and outside the biotech industry. It does because, on the surface, it is innocuous. Indeed, what bad can come from understanding the science in detail? Multiple issues arise, however, when investors and corporate portfolio managers try to follow the scientific narrative.

One issue was already mentioned: more information does not always mean better information. Additionally, decision-makers often pressure scientists to definitively interpret the scientific data, even when such interpretation cannot exist. Scientists often comply. Even worse, experienced R&D managers often pre-emptively overstate the definitiveness of their findings, knowing that this is what the financial decision-makers expect.

Deterministic thinking

Is overconfidence all bad then? The Inventor: Out for Blood in Silicon Valley is a 2019 documentary film that explores this dark side of the Silicon Valley startup culture. It paints the Fake it till you make it mindset as the culprit, which enabled the meteoric rise and sharp fall of Theranos, turning it into the most scandalous name in biotech history. However, the film also makes a subtler point that without overconfidence, there would be not only no Theranos, but also no Apple, no SpaceX, and perhaps no incandescent lightbulb.

Dan Ariely, a renowned behavioral economist, brings up this idea several times throughout the film: “I wouldn’t want to live in a society where people are not overconfident in what they can achieve. Who would open a restaurant?” And later, “So the reality is that data doesn’t sit in our minds the way that stories do. […] Even more importantly, stories have [the] emotion that data doesn’t. And emotions get people to do all kinds of things: good and bad.”

Navigating Uncertainty with Heuristics

So how do we use our overconfidence and storytelling ability for good? And for those of us holding the purse strings, what are the signs to look for?

Credible scientific thesis

Should our primary focus be on the markets or science?

Early-stage venture capitalists argue that product vision should supersede financial projection in young companies. In Bruce Booth’s words: “No drug discovery stage startup needs to have a market model […] instead they need to have a credible thesis for how they will address an important medical issue […]”.

But what does it mean to have a credible thesis? After all, the amyloid hypothesis was a highly credible approach to Alzheimer’s Disease treatment. So much so that it famously prevented the decision-makers from exploring alternative ideas, resulting in lost decades and wasted billions. Personalized medicine is another cautionary tale of how a convincing scientific narrative can lead someone to underappreciate or overlook other contributing factors.

As a former bench scientist, I cannot argue with the need for a sound scientific rationale. There needs to be a conviction among scientists and entrepreneurs to attract funding and move the project forward. But if it is the entrepreneur’s job to build and exhibit that conviction, what is left to do for an investor?

Investor’s job (alpha)

Some might argue that it is the investor’s job to add alpha. In finance, alpha is defined as a measure of active return, i.e. a degree of investment outperformance in comparison to the other assets in its market. One way an investor can add alpha is by picking drug projects with a higher than average R&D success probability. Over the past two decades, several heuristics emerged as markers of such increased success likelihood.

Heuristics

AstraZeneca provides an excellent account of heuristic signals, identified through a historical intra-organizational project survey. In its Nature publication, their team reports the following five factors:

- The right target

- The right patient

- The right tissue

- The right safety

- The right commercial potential

Of these, arguably, the most powerful is the first. AstraZeneca reported a two-fold increase in the probability of drug approval in instances when there was a genetic association between the chosen pharmacological target and disease occurrence.

On top of the above factors, investors can stack non-technical signals, such as Academic Pedigree, Market & Competition, Intellectual Property, Regulatory Landscape, to try gaining additional predictive power.

Alpha? More like beta

However, the problem with using that classical, heuristics-based approach is that not only the signals above are noisy and qualitative, but they are also well known and tend to come at a very high premium. Indiscriminate buying of these factors leads to the dramatic overvaluation of biotech securities, particularly during economic booms.

Indeed, one would think that biotech companies are purely scientific risk bets. As such, they should be uncorrelated from the broader market, i.e. exhibit a low market beta. However, NYU Stern clocks the average beta for the biotechnology industry at 1.43. In fact, is not uncommon for biotech companies to have betas above 2.

A variety of possible explanations exist. For example, Andrew Lo, a renowned financial economist, proposed that the high industry beta reflects the constant need for biotechs to raise capital to fund R&D. Thus, biotech as an industry depends on the broader economy for funding. Whether or not you subscribe to that view, you probably will agree that investor risk appetite varies dramatically through time. As a risky industry, biotech is naturally taking a lot of capital inflows when things are good and a lot of outflows when things get scary, thus becoming strongly correlated with the overall economic outlook.

The overvaluation is likely even worse in private markets, in which there are no short-selling pressures and virtually no liquidity, i.e., no opportunity for a sell-off during a market downturn. Furthermore, because there is a trend toward preclinical and early clinical stage IPOs, private investors take on less idiosyncratic risk as well. In general, comparative human trials are only employed when the uncertainty about the drug’s efficacy is maximal. Thus, the main R&D risks are addressed in middle and late clinical development (Phase 2 and 3), when the company has typically gone public already.

Let’s review. On the one hand, private biotechs give an impression of low volatility and low market correlation, as neither is directly observable in private markets. On the other, there is a possibility of an early exit either via a trade sale or an IPO, before the main R&D risks (Phase 2 and 3) materialize. A combination of these factors led to the immense popularity of venture-stage biotech investments. Over 40% of venture capital funding reportedly goes to preclinical companies. But one has to wonder about the degree to which such investments are a source of an active (alpha), or passive (beta) return? More importantly, since these dollars are not engaging with the main R&D risks in a meaningful way, are such investments a good use of our resources from a societal perspective?

Navigating Uncertainty with Probabilistic Models

So, far I mainly berated the discretionary, heuristics-based approach to biotech investing. But what does the alternative look like?

The megafund model

In their 2012 Nature Biotechnology article, Fernandez, Stein, and Lo introduced a probabilistic model of biotech finance. This model informed the investment theses behind biopharma powerhouses, like BridgeBio and Roivant, which have raised 8 and 9-digit investment rounds from biotech-agnostic VC/PE behemoths, like SoftBank and KKR.

Probabilistic models

To understand what such probabilistic models estimate, we need to go back to our McKinsey equation in Figure 1. Let’s dispense with the accounting terminology and rewrite it here in biotech parlance:

R&D productivity = Commercial potential x R&D success probability and timing

R&D Costs

The problem with deterministic models is that they provide little information on the error surrounding the estimate of the numerator of the right side of the equation. Discretionary investors flock to heuristics that lead them to overestimate the numerator and commit additional resources in the denominator, driving the resulting R&D productivity down.

Probabilistic models aim to use historical data to estimate both the central tendency and the uncertainty surrounding the R&D productivity drivers in the above equation.

Models of R&D uncertainty

Having such models would enable investors to engage with R&D risks in a way that actually generates alpha and promotes ESG principles. Because there are no predictive models of R&D success, both corporate and financial investors tend to gravitate towards the aforementioned heuristics when allocating their capital. As discussed above, there is some evidence that such heuristics have predictive value. But the downside of excessive reliance on heuristic signals is that a vast number of projects that do not exhibit them get overlooked and underfunded. For example, I believe one of the reasons that the amyloid hypothesis seemed so attractive as a potential treatment modality for Alzheimer’s Disease was that aberrations in the gene that codes for its therapeutic target, the Amyloid Precursor Protein, were highly associated with the disease occurrence. Does that generic association indicate that targeting this protein might be the right path to the treatment? Of course, it does. But how many alternative strategies were overlooked because they did not exhibit such obvious genetic association.

Models of commercial potential

The valuation of biotech assets depends on the magnitude of future drug sales, which are themselves subject to high uncertainty. While the uncertainty of R&D outcomes has been described and modeled in the literature to a degree, the uncertainty of drug sales is far less understood in my opinion. Additionally, biotech asset valuation depends on the current supply/demand levels of the innovation market. These factors vary through time and space, depending on the current competitive landscape and macroeconomic environment.

Because there are no predictive models of a drug’s commercial potential, investors tend to rely on the same heuristics, which are used to estimate the R&D success likelihood, to gauge value. This leads to a compounding of errors and further overvaluation of assets, particularly in opaque, private markets. The tendency to overpay for a perception of reduced uncertainty is especially apparent at the later stages of private financing, as the less discerning and more deep-pocketed investors start entering the cap table.

The Indeterminate Optimistic Future

In his iconic SXSW talk, Peter Thiel’s proposes that the future can be modeled as a 2×2 matrix. He argues that the future is seen as either determinate, or indeterminate; and optimistic, or pessimistic. And that the optimal course of action depends on which quadrant you are in on that matrix.

For example, if future is uncertain, diversification dominates conviction as a resource allocation strategy:

Figure 3. Peter Thiel Sees the Future in 2×2 Matrices

Or if future becomes optimistic, investors become more risk averse:

Figure 4. Peter Thiel 2×2 Matrix (Optimism vs. Pessimism)

He also talks about the evolutionary dominance of certain industries and disciplines that naturally emerges as the future shifts from one quadrant to another:

Figure 5. Peter Thiel 2×2 Matrix (Industries and Disciplines)

I believe such a shift is now happening in the biotech industry. As the information becomes more complex and fragmented, the investors need to become more systematic and probabilistic in their view. Our job is to integrate the fragment data using quantitative methods and use the resulting models to allocate our capital in concordance with potential risk and reward. Even though the future of biotech is becoming less determinate, it remains optimistic. Thus, we should strive to financially incentivize innovation to reflect its future societal value and use financial markets to arbitrage away capital misallocation.

The Blog

In the following series of blog posts, I provide data-driven insights about the evolution of the biotech industry and speculate about the role of an active biotech investor in its future.

I begin by outlining the basic analytical framework in three sections:

UNDER CONSTRUCTION

- The risk-side of drug development

- The reward side (Bayesian Model of Drug Commercialization Uncertainty)

- Putting it all together (Combined Model of Biotech Innovation Profitability)